Login

Login

Appraisal fee and due date changes – are these impacting your financial and operational performance?

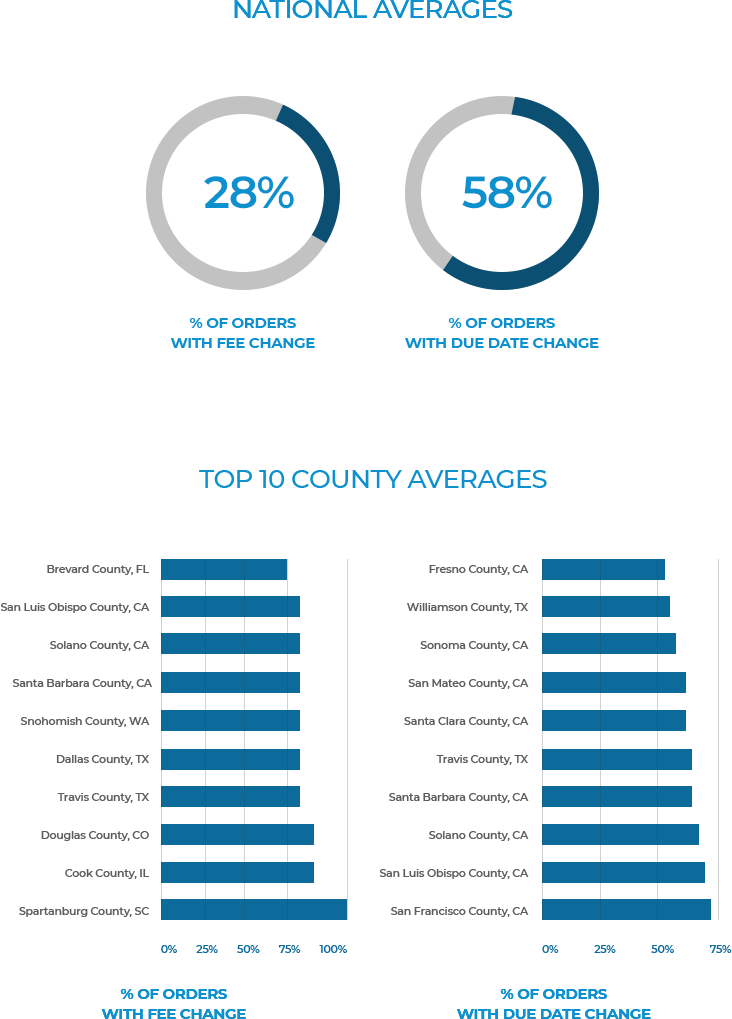

It goes without saying, there has been a dramatic increase in the number of appraisal orders with fee increases and/or due date changes following the initial placement of the order. This has led to frustration amongst borrowers, lenders, and brokers.

In some counties, the percentage of orders with fee increases and/or due date changes has reached 70%. If you drill down further, some zip codes have fee and due date adjustments on 100% of the orders placed.

Fee increases and due date changes cost lenders time and money. For an appraisal order with a fee increase, lenders are seeing an average increase of $200 per order, and thus a 4.5 day increase in turn time. Considering that fee changes are not a valid change in circumstance, that $200 per order is coming right off the lenders bottom line, and leaves customers waiting on their appraisal with a poor experience.

How did we get here, and more importantly, how do we fix it?

What caused the dramatic increase in fees and due date changes?

The simple answer is volume and reporting. The reality is the current processes and systems used by lenders and AMCs are simply not capable of identifying an accurate fee and turn time at the point of sale.

Many lenders have attempted to solve the issue by first increasing the number of AMCs they use, or secondly, increasing their appraisal fees, or both. Neither approach solves the problem. In fact, it often does the opposite, and adds to the trouble with increases in vendor management and operational costs for the lender. AMCs often pull from the same pool of appraisers, so adding more AMCs does not always expand coverage since many appraisers are on multiple AMC panels. Increasing fees seems logical, but that means the borrower is paying more, and if the AMC does not have coverage in the area, the fee could still go up and take longer to fulfill. Furthermore, offering more money to appraisers does not guarantee a faster turnaround, given that it opens the door for appraisers to accept orders in an area they are unfamiliar with or need to drive a longer distance to reach.

For AMCs, it is crucial that they have appraiser coverage in markets where lenders originate. Current AMC systems and allocation models do not provide the necessary transparency for a lender to make an informed decision at the time the order is being placed. So, what is the real solution?

Modernizing and connecting a fragmented ecosystem.

To fully tackle this supply chain problem, lenders need to inject actionable analytics into the process at the point of sale. In other words, bring vendor and order management together in a single platform creating a real time data-driven supply chain.

With a multi-tenant platform that combines business intelligence and order management in a single instance, market participants can seamlessly interact, share data, and simplify the delivery of any valuation product. By doing so, all market participants will realize increased margins, lower operating costs, and an improved customer experience.

Interested in learning more?

Visit us at appraisalvision.com or contact us at info@appraisalvision.com for more information.

Related posts

{kind=link}